Improving Cred App

Improving Cred App

A comprehensive analysis of the Cred app’s core value proposition to improve app's User Retention.

Project Overview

Cred app is proudly embellishing the Indian Startup Indian Unicorns List. The app also went popular among the Indian masses after its IPL promotions. Originally I could not understand the hype around the app and it was targeting the top 1% of India — a segment I hadn’t worked with. So I took this challenge to improve the app that was completely out of my league.

Cred App encourages its users to pay their credit cards on time by throwing reminders. It rewards its users with offers from premium brands for every payment through the app. It comes with other product offerings-

Cred RentPay- It helps users pay their rent using credit cards. They get some benefits for in-app payments.

Cred Stash- It gives personal loans to the Cred community with an interest rate of about 15. 5% with extra processing charges.

Cred Mint- It is an investment product where the Cred community can invest money and earn interest of 9%. The money is used to lend credit-worthy Cred members via Cred Cash.

Cred Store- A marketplace offering premium brands.

Cred Protect- Helps users understand credit card statements and their spending patterns.

The app rewards the creditworthy and affluent. It aims to bring all these people together and help each other. Thus it allows people who have an Experian score above 750 to be part of the Cred community. As of 2021, the community is sized 7.5 million.

Revenue Model

Listing Fees: Earns revenue through the listing fees charged from premium brands that sell on their platform.

Transaction and processing fees: It charges a processing fee of around 1 to 1.5% on transactions made through the platform.

Goal: The platform is looking to acquire users to form a community of creditworthy. Our solution must also help in user retention since user acquisition and retention are interrelated.

User retention is the new user acquisition.

The cost of gaining a new user is more than the cost of making a user stay. If we are able to convince users to stay, they will help us in bringing new users without cost, and the community formed could be stronger. Thus our goal will be to acquire new users and retain existing users in the platform.

Research

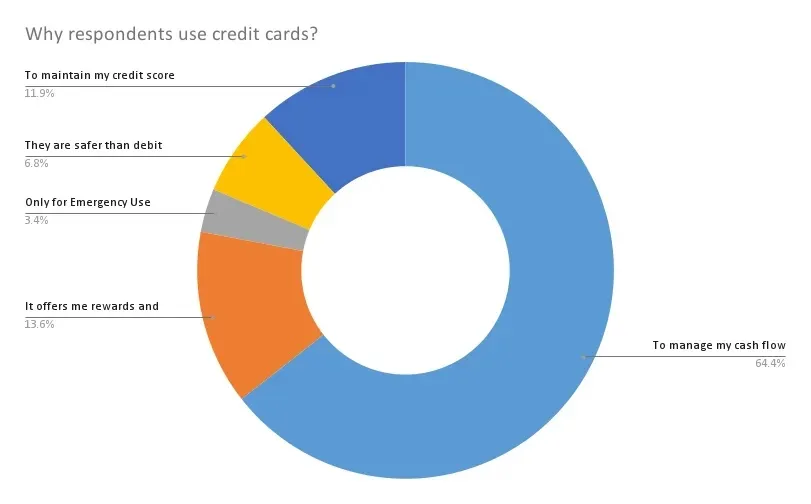

Primary research: I conducted a survey with 75 participants who had at least one credit card and they mostly identified themselves as upper-middle class. One of the pivotal insights we obtained from the survey was ‘Why do people use credit cards?’

64.4% use credit cards to manage their cash flow.

13.6% use credit cards to get rewards.

11.9% use credit cards to maintain credit scores.

6.8% feel credit cards are safer than debit cards to use.

3.4% use credit cards for emergency.

Secondary Research: User reviews on play store and third-party sites were my crucial source of information. Major issues reflected in the user data are as follows

Delay in transactions.

No proper customer support.

No responsibility is held for buying offers from the platform.

Cred gets access to the email linked to the bank account to get statements and due dates. This has lots of privacy concerns.

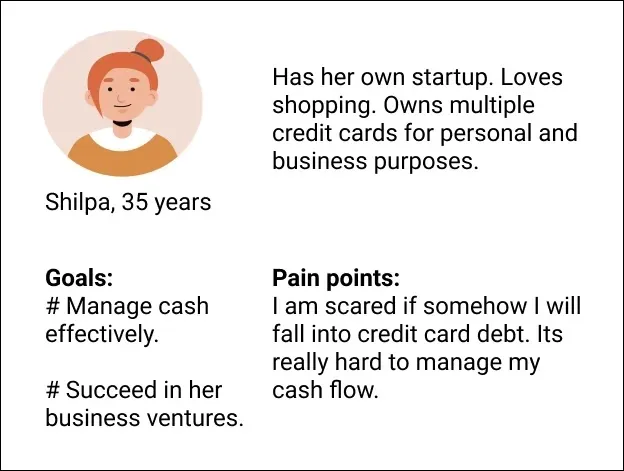

User Personas

Credit card users can be classified as individual and business credit card users. In our case study, we focus on individual card users.

Problem understanding

Cred is not actually solving a real user problem as of yet for the reason that people already get rewards for paying their credit card bills on due from banks. More rewards are definitely not a user problem.

Cred also allows people to be mindful of their credit card payment dues but these people already are financially disciplined as they are to be deemed creditworthy to be part of the community. Sub-optimal solutions are not always a pain point. It is similar to schools only taking in top scorers and boasting that they make topers.

Cred possibly wants to create a new behavior and connect people, utilize the network effects to its advantage. The platform can be considered a two-sided marketplace or a bandwagon social network. More card users on the platform will result in more premium brands which might lead to even more cards users. It also can be considered a bragworthy proposition (As quoted by the CEO). I consider it an imperfect network as Cred is not the Amazon of premium brands because they do not take responsibility for the product after it is bought(or redeemed) in the platform. The network is unsustainable since the core value proposition does not revolve around the network but rather an addon. Social networks built on user reputation need to recreate themselves frequently to remain in the buzz.

Another issue is that getting out of the app is a lengthy process that involves contacting the support team. Often times there are cases where people simply uninstall the app without following the process and their data is still held within the app. This could mislead us and there might be a missed customer. As far as we know the app has successfully onboarded 7.5 million users out of 10 million app downloads but we don’t know how many of them are retained.

The app has also faced criticism for spending too much on marketing to acquire users without generating adequate revenues.

Solution

A strong reason to enter the app is key to acquisition and retention.

We noticed that the Cred app was not convincing enough at least not in the long run. With a slight twist in the way how Cred works, we will be able to acquire new users and solve a real problem.

Let’s dive into a key understanding regarding the user’s motivation to enter the app. Which one would you prefer?

Your professor(or teacher) rewards you with chocolates every day for being punctual in class.

Your professor gives your attendance even when you come late to class one day since he lets it slide this one time because you were punctual before.

We always do good deeds in hope of reaping fruits in the future even when they are difficult to follow. People maintain credit scores for similar reasons- to get better credit in the future. In our case the chocolates metaphorically denote rewards and the attendance denotes security. Here we are dealing with people who are managing cash on an everyday basis. Thus security will definitely be a strong motivator for them to use the app since when it comes to money people always opt for security more than rewards.

The main problem credit card users face is credit card debt and cash flow management. If we could offer them a way to ease their credit card debt on their rough day we will be able to make a strong motivator. Let’s see some ways we could solve the problem.

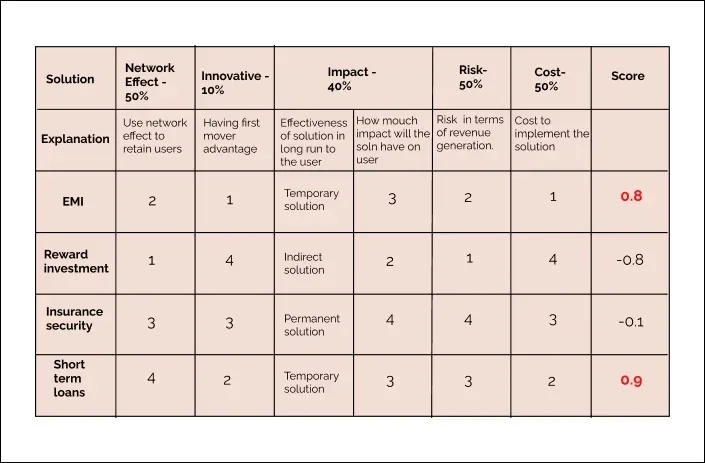

Loans to convert credit card dues to EMI instantly (extending Cred stash).

Reward investments instead of (or including) premium brand offerings.

Provide an insurance security cover for a credit card due payments under certain terms and conditions. (Probably illogical)

Provide very short-term instant loans and very short-term investment vessels to transact money from peers.

We have prioritized EMI and short-term loans from the four solutions. EMI and Short term loans had relatively lower costs and risks. The prioritized solutions also are effective in boosting network effect, innovative service in India, and are very impactful.

Stakeholders

Users

Short-term loans and investments will be a good way for users to manage cash flow. Instant EMI will help users make a quick transition from credit card to EMI reducing the tedious process.

Platform

Implementing the prioritized solution will increase in user acquisition and retention.

Interest Calculation

We could optimize the interest for a loan by maximizing profit and minimizing default risk.

Decision variable: Interest rate (The interest rate here is not annual)

Key factors

Loan Amount

Inflation

Credit score

Loan Duration

Buying habits.

Constraints

(Inflation)/12 < Interest rate

Credit score > 750

Objective functions

Profit = (Loan Amount * Interest rate ) / (Loan Duration * (Inflation/360) )

Default risk = (Loan amount * Interest rate ) / (Credit Score)

Note: The above functions are empirical and give an idea about profit and not the exact value.

Project Images

Project Claps

Recent Clappers

Showing 5 of 5 clappers

Discussion

Please log in to join the discussion.